Table of Contents

I. Introduction to Project Cost Management

A. Understanding the Importance of Cost Management in Projects

Project cost management plays a pivotal role in the success of any project. It involves the planning, estimating, budgeting, and controlling of costs to ensure that the project is completed within the allocated budget. Effective cost management is not just about keeping expenses in check; it also helps in optimizing resource utilization, reducing wastage, and enhancing overall project efficiency. By closely monitoring and managing costs, project managers can make informed decisions, avoid cost overruns, and ensure that the project remains financially viable.

Key Points

Cost management is a critical aspect of project management that holds immense importance for successful project delivery. Here are the key reasons why cost management is crucial in projects:

- Budget Control: Cost management ensures that projects are completed within the approved budget. It involves estimating, allocating, and monitoring expenses to prevent cost overruns that can disrupt project progress and strain resources.

- Resource Optimization: By effectively managing costs, project managers can optimize resource allocation. They can identify areas of resource inefficiencies, eliminate wasteful spending, and allocate resources to activities that contribute most to project objectives.

- Risk Management: Cost management includes setting aside contingency reserves to address potential risks and uncertainties. This proactive approach prepares projects for unexpected events, minimizing their impact on project outcomes.

- Decision-Making Support: Cost management provides real-time data on cost performance. Project managers can make informed decisions based on cost metrics such as Cost Performance Index (CPI) and Cost Variance (CV), enabling them to take timely corrective actions.

- Client Satisfaction: Staying within the budget and delivering value for money enhances client satisfaction. Transparent cost management practices build trust with stakeholders and strengthen relationships with clients.

- Project Viability: Proper cost management contributes to the project’s viability. Well-defined budgets and cost estimates improve the chances of project approval and funding, securing support from key stakeholders.

- Financial Health: Successful cost management positively impacts an organization’s financial health. It helps minimize unnecessary expenses and increases the likelihood of generating profits from projects.

- Competitive Advantage: Organizations that excel in cost management gain a competitive edge. They can offer competitive prices in bids, attracting more clients and opportunities for growth.

- Project Performance Assessment: Cost management metrics provide valuable insights into project performance. They facilitate performance assessment and enable project managers to assess progress against planned costs.

- Sustainable Project Success: Cost management contributes to sustainable project success. By ensuring financial discipline and efficient resource utilization, it enhances the overall project outcome and contributes to the organization’s long-term success.

In conclusion, cost management is more than just tracking expenses; it is a strategic approach that impacts various facets of project execution. Effective cost management leads to better budget control, optimized resources, proactive risk mitigation, and ultimately, the successful delivery of projects that meet client expectations and organizational objectives.

B. The Impact of Effective Cost Management on Project Success

Effective cost management has a significant impact on the success of a project. When project costs are managed well, it leads to better cost predictability, allowing stakeholders to plan and allocate resources more effectively. This, in turn, enhances the overall project performance and helps in meeting project objectives within the agreed-upon budget and timeline. Additionally, successful cost management fosters client satisfaction, as they receive the desired project outcomes without unexpected financial burdens. It also strengthens the organization’s financial health by minimizing wasteful expenditure and increasing the chances of generating profits from the project.

Key Point: Effective cost management has a significant impact on the success of a project. It involves careful planning, monitoring, and controlling of project expenses to ensure that the project is completed within the allocated budget. The following are the key impacts of successful cost management on project success:

- Budget Adherence: Proper cost management ensures that the project stays within the approved budget. This allows stakeholders to allocate resources efficiently and minimizes the risk of cost overruns, which can jeopardize the project’s financial viability.

- Resource Optimization: By closely monitoring costs, project managers can optimize resource utilization. They can identify areas of resource inefficiencies, eliminate wasteful spending, and allocate resources where they are most needed, leading to enhanced project efficiency.

- Timely Decision Making: Effective cost management provides project managers with real-time data on cost performance. This enables timely decision-making, allowing them to address cost-related issues promptly, such as reevaluating resource allocation or adjusting project scope.

- Client Satisfaction: Delivering the project within the agreed-upon budget enhances client satisfaction. Clients appreciate the transparency and accountability that effective cost management brings, ensuring they receive the expected outcomes without unexpected financial burdens.

- Financial Health: Successful cost management positively impacts the organization’s financial health. Minimizing unnecessary expenses and maximizing project value increase the likelihood of generating profits from the project.

- Risk Mitigation: Proper cost management includes setting aside contingency reserves to manage potential risks and uncertainties. This prepares the project for unforeseen events, reducing the impact of risks on project outcomes.

- Competitive Advantage: Organizations that excel in cost management gain a competitive edge. They can bid competitively on projects, attracting more clients and opportunities for growth.

- Project Viability: Projects with well-managed costs are more likely to be approved and funded by stakeholders. Demonstrating a clear cost management strategy enhances project viability and support.

- Performance Assessment: Cost metrics, such as Cost Performance Index (CPI) and Cost Variance (CV), provide valuable insights into project performance. These metrics help identify areas of concern and enable corrective actions to be taken to keep the project on track.

In conclusion, effective cost management is not just about avoiding cost overruns; it is a strategic approach that influences project success in multiple ways. By adhering to budgets, optimizing resources, ensuring client satisfaction, and mitigating risks, organizations can achieve successful project outcomes and strengthen their overall project management capabilities.

C. Key Cost Management Terminologies and Concepts

To navigate the world of project cost management, understanding key terminologies and concepts is vital. Some essential terms include:

- Cost Baseline: The approved budget against which project performance is measured.

- Cost Estimation: Determining the approximate costs of project activities and resources.

- Cost Variance: The difference between the budgeted cost and the actual cost incurred.

- Earned Value Management (EVM): A technique to assess project performance by comparing planned progress, actual progress, and the associated costs.

- Contingency Reserve: An amount set aside to cover potential risks and uncertainties.

- Life Cycle Costing: Considering the total cost of a project over its entire lifecycle, including operational and maintenance expenses.

Understanding these terminologies empowers project managers to make informed decisions, communicate effectively with stakeholders, and manage costs proactively throughout the project’s life cycle.

Example: Let’s consider a construction project to build a new office building. Effective cost management involves accurately estimating costs for labor, materials, and equipment, creating a cost baseline, and continuously monitoring expenses against the budget. Suppose the project manager identifies potential risks, such as weather delays, material price fluctuations, or scope changes. In that case, they allocate contingency reserves to handle unforeseen situations. By doing so, they can navigate challenges while ensuring the project remains within budget and meets the stakeholders’ expectations. This exemplifies how proper cost management contributes to the success of the project.

II. Project Cost Estimation Techniques

Accurate cost estimation is crucial for effective project planning and budgeting. Various techniques are employed in project cost estimation, each catering to specific project requirements. The following are the three primary cost estimation techniques:

A. Analogous Estimating: Leveraging Historical Data

Analogous estimating, also known as top-down estimating, relies on historical data from past projects to estimate the costs of current projects. This technique assumes that projects with similar characteristics and scope will have comparable costs. Project managers use data from previous projects as a reference point to estimate costs for the current project. Analogous estimating is particularly useful during the early stages of a project when limited information is available. It provides a quick and simple way to derive ballpark figures for budgeting and preliminary planning.

Key Points:

- Uses historical data from similar past projects as a basis for estimation.

- Provides quick and approximate cost estimates.

- Suitable for projects with limited details and early in the planning phase.

Example: In a construction company, a project manager is tasked with estimating the costs for building a new office complex. The manager reviews data from past office building construction projects that have similar size, design, and scope. By comparing the historical project costs, the manager estimates the approximate expenses for the current project. This analogous estimating allows the team to present an initial budget to the stakeholders, enabling them to make informed decisions at the project’s outset.

B. Parametric Estimating: Mathematical Models for Estimation

Parametric estimating involves using statistical relationships and mathematical models to estimate project costs. This technique uses historical data and relevant project parameters to develop cost estimates. The parameters can include cost per unit, cost per square foot, or cost per hour, depending on the nature of the project. By establishing a correlation between the project’s characteristics and the associated costs, project managers can calculate estimates with greater accuracy. Parametric estimating is best suited for projects with well-defined components and clear quantifiable variables.

Key Points:

- Utilizes mathematical models and statistical relationships for estimation.

- Requires clearly defined parameters and variables for accuracy.

- Offers greater precision in cost estimation for specific project components.

Example: A software development company is embarking on a new software development project. The project manager uses parametric estimating by analyzing data from past software development projects, such as cost per line of code, development time per feature, and defect rate. By considering the parameters and applying the established mathematical models, the project manager accurately estimates the time and cost required for the current project, facilitating better resource planning and budget allocation.

C. Bottom-Up Estimating: Detailed Analysis for Accurate Estimates

Paragraph: Bottom-up estimating, also known as detailed estimating, involves breaking down the project into smaller work packages and estimating the costs for each individual component. Project managers work closely with subject matter experts to determine the cost of every task, material, labor, and equipment required. These detailed estimates are then aggregated to calculate the overall project cost. Bottom-up estimating offers a highly accurate cost estimation method, particularly for complex projects with well-defined tasks and deliverables.

Key Points:

- Breaks down the project into granular work packages for estimation.

- Requires collaboration with subject matter experts for detailed cost assessment.

- Provides the highest level of accuracy in cost estimation.

Example: A construction project manager is tasked with estimating the cost of building a new bridge. The manager collaborates with architects, engineers, and contractors to develop detailed estimates for every aspect of the project, including materials, labor hours, equipment rental, and specialized construction techniques. By combining these granular estimates, the project manager arrives at a comprehensive and precise cost estimate for the entire bridge construction project.

In conclusion, project cost estimation techniques play a vital role in project planning and budgeting. By employing the appropriate estimation technique based on project characteristics and available data, project managers can make well-informed decisions, set realistic budgets, and ensure successful project delivery.

III. Developing a Comprehensive Cost Baseline

A. Creating the Project Budget: Allocating Resources and Costs

Creating a comprehensive project budget is a crucial step in cost management. It involves identifying all the necessary resources, both human and material, and estimating the associated costs. The project manager collaborates with relevant stakeholders to determine the budgetary constraints, funding sources, and financial goals for the project.

Key Points:

- The project budget is a detailed financial plan that outlines the total estimated cost for executing the project.

- It includes direct costs, such as labor, materials, and equipment, as well as indirect costs like administrative expenses and overheads.

- A well-structured budget enables effective resource allocation and helps prevent cost overruns.

Example: In a software development project, the project manager collaborates with the development team, procurement department, and finance team to identify the resources needed. They estimate the costs for software licenses, development hours, testing equipment, and other necessary expenses. By consolidating these estimates, the project manager creates a project budget, ensuring that all costs are accounted for.

B. Contingency Reserves: Preparing for Unforeseen Expenses

Despite careful planning, unexpected events or risks may arise during the project’s execution. To address such uncertainties, a contingency reserve is set aside within the project budget. Contingency reserves act as a financial safety net, providing a buffer to cover unforeseen expenses without impacting the project’s primary budget.

Key Points:

- Contingency reserves are contingency funds that are allocated as a percentage of the overall project budget.

- They are used to handle risks and uncertainties that were not accounted for in the initial cost estimation.

- Contingency reserves should be managed judiciously to avoid unnecessary utilization.

Example: In a construction project, a project manager includes a contingency reserve of 10% of the total budget to accommodate potential weather delays or price fluctuations of construction materials. This reserve helps to address any unforeseen challenges that may arise during the construction process without exceeding the approved budget.

C. Cost Management Plan: Outlining Cost Control Strategies

The cost management plan is a crucial document that outlines the strategies and procedures for managing, monitoring, and controlling costs throughout the project lifecycle. It provides clear guidelines on how costs will be managed and how variances from the baseline will be addressed.

Key Points:

- The cost management plan defines the roles and responsibilities of team members related to cost management activities.

- It includes cost performance metrics, such as Cost Performance Index (CPI) and Cost Variance (CV), to measure the project’s financial health.

- The plan also outlines the process for approving changes to the project budget and ensures proper communication with stakeholders regarding cost-related matters.

Example: In a marketing campaign project, the cost management plan outlines the procedures for tracking expenses, comparing actual costs against the budget, and assessing cost performance using established metrics. It also specifies how any cost deviations will be addressed, and the stakeholders will be informed and involved in decisions related to cost changes.

Developing a comprehensive cost baseline is vital for project success. By creating a well-defined project budget, establishing contingency reserves, and outlining effective cost management strategies, project managers can ensure financial control, mitigate risks, and enhance the overall project outcome.

IV. Cost Control and Monitoring

A. Earned Value Management (EVM): Measuring Performance Against Budget

Earned Value Management (EVM) is a powerful cost control technique that enables project managers to assess the project’s performance in terms of both schedule and budget. It integrates information on planned work, actual work completed, and the associated costs. EVM provides valuable insights into the project’s progress and financial health, allowing early identification of potential cost overruns or schedule delays.

Key Points:

- EVM compares the Earned Value (EV), which represents the value of completed work, to the Planned Value (PV), which is the planned cost of work scheduled.

- The Cost Performance Index (CPI) and Schedule Performance Index (SPI) are key EVM metrics used to assess cost and schedule performance, respectively.

- A CPI greater than 1 indicates that the project is performing better than planned in terms of cost, while an SPI greater than 1 suggests that the project is ahead of schedule.

Example: In a software development project, the project manager regularly analyzes the EVM metrics. If the CPI is 1.2, it means that the project is completing work at 20% less cost than planned, indicating good cost control. Similarly, if the SPI is 1.1, the project is ahead of schedule by 10%, demonstrating efficient time management.

B. Variance Analysis: Identifying Deviations and Corrective Actions

Paragraph: Variance analysis is a technique used to identify deviations between planned and actual project performance. By comparing actual costs to the baseline budget, project managers can detect cost variances and investigate the reasons behind them. Variance analysis allows for timely corrective actions to bring the project back on track and prevent cost overruns.

Key Points:

- Positive variances (favorable) occur when actual costs are less than planned, indicating efficient resource utilization.

- Negative variances (unfavorable) occur when actual costs exceed planned costs, necessitating cost control measures.

- Variance analysis is an ongoing process that enables continuous monitoring and adjustment to ensure project success.

Example: In a construction project, if the actual costs for materials and labor are higher than the planned costs, the project manager conducts variance analysis to understand the reasons behind the cost increase. It could be due to price fluctuations or inefficient resource management. Based on the findings, appropriate corrective actions, such as renegotiating supplier contracts or optimizing workforce utilization, are implemented.

C. Change Control: Managing Scope Creep and Its Impact on Costs

Scope creep refers to uncontrolled changes or additions to the project scope that can impact project costs. Effective change control processes are essential to manage scope changes and their potential financial implications. Change control involves evaluating proposed changes, assessing their impact on the project budget, and obtaining approval before incorporating them into the project.

Key Points:

- A Change Control Board (CCB) is typically established to evaluate and approve or reject proposed changes based on their impact on project objectives, timeline, and budget.

- Unapproved changes can lead to cost overruns, resource inefficiencies, and schedule delays, making change control vital for cost management.

Example: In a marketing campaign project, if the client requests additional deliverables beyond the original scope, the project manager involves the CCB. They assess the impact on the project budget and timeline before making a decision. By implementing robust change control processes, the project manager ensures that the project remains within budgetary constraints and prevents uncontrolled scope changes from affecting project costs.

Cost control and monitoring are integral to project success. Through Earned Value Management, variance analysis, and effective change control, project managers can maintain financial discipline, detect deviations early, and take corrective actions to deliver projects within budget while achieving project objectives.

V. Leveraging Cost-Benefit Analysis

A. Evaluating Project Benefits: Quantitative and Qualitative Factors

Paragraph: Cost-benefit analysis is a vital technique that helps project managers assess the potential benefits and drawbacks of a project. It involves evaluating both the quantifiable (quantitative) and non-quantifiable (qualitative) factors to determine whether the project is financially viable and aligns with the organization’s strategic goals.

Key Points:

- Quantitative factors include monetary values that can be measured in financial terms, such as revenue generation, cost savings, or increased efficiency.

- Qualitative factors are non-monetary aspects that contribute to the project’s value, such as improved customer satisfaction, brand reputation, or employee morale.

Example: In an IT infrastructure upgrade project, the quantitative benefits may include reduced maintenance costs, increased processing speed, and enhanced data security. Qualitative benefits could include better user experience, reduced downtime, and increased employee productivity, which contribute to overall project success.

B. Identifying Cost Drivers: Optimizing Resources for Maximum Value

Cost drivers are factors that significantly influence project costs. Identifying these drivers helps project managers allocate resources effectively to maximize project value while controlling expenses. Analyzing cost drivers allows managers to prioritize resources for tasks with the most significant impact on project success.

Key Points:

- Identifying cost drivers involves understanding which project activities or resources have the most substantial effect on the project’s overall cost.

- By focusing resources on activities with high impact, project managers can optimize project outcomes and ensure efficient resource allocation.

Example: In a manufacturing process improvement project, the cost drivers may include labor costs, raw material expenses, and equipment maintenance. The project manager allocates resources strategically, investing in automation to reduce labor costs and optimizing the use of raw materials to minimize wastage, effectively managing cost drivers.

C. Decision-Making with Cost-Benefit Analysis: Making Informed Choices

Paragraph: Cost-benefit analysis equips project managers with crucial information to make informed decisions about project feasibility, prioritization, and resource allocation. By comparing project costs against the potential benefits, project managers can determine the best course of action and justify investment in the project.

Key Points:

- Cost-benefit analysis supports data-driven decision-making, ensuring projects align with the organization’s strategic objectives and financial constraints.

- It helps identify projects with high returns and justifies the allocation of resources to initiatives that yield the most significant benefits.

Example: In a software development company, the project manager uses cost-benefit analysis to evaluate multiple projects. They select the project with the highest potential return on investment, as it aligns with the company’s growth strategy and financial goals, ensuring optimal resource allocation.

Leveraging cost-benefit analysis empowers project managers to make well-informed decisions, optimize resource allocation, and prioritize projects that align with organizational goals. By evaluating both quantifiable and non-quantifiable factors, cost-benefit analysis provides a comprehensive view of a project’s potential benefits, allowing for effective project selection and resource optimization.

VI. Procurement Management and Cost Considerations

A. Procurement Planning: Aligning Procurement Strategy with Project Objectives

Procurement planning is a crucial aspect of project cost management, focusing on acquiring necessary resources and services from external vendors. It involves aligning the procurement strategy with the project’s objectives to ensure cost-effectiveness and timely delivery of goods and services.

Key Points:

- Procurement planning involves identifying what needs to be procured, when it is required, and from whom.

- By carefully planning procurement, project managers can avoid delays caused by late deliveries and ensure that the project stays on schedule.

- An effective procurement strategy considers factors such as budget constraints, quality requirements, and risk mitigation.

Example: In a construction project, the project manager identifies that specific materials, like steel beams, will be required at a later stage. They plan procurement accordingly, ensuring that the materials are ordered well in advance to avoid construction delays.

B. Contract Types: Understanding Cost Implications and Risks

Choosing the right contract type is essential for managing project costs and risks. Different contract types carry varying degrees of financial responsibility and risk allocation between the buyer and the seller.

Key Points:

- Fixed-Price Contracts: These contracts set a specific price for the deliverables, shifting most of the risk to the vendor. They are suitable for well-defined projects with minimal changes.

- Cost-Plus Contracts: In these contracts, the buyer reimburses the vendor’s costs and adds a predetermined fee. They are more flexible for projects with evolving requirements.

- Time and Material Contracts: These contracts pay vendors based on the hours worked and materials used. They are suitable for projects with uncertain or changing scope.

Example: For a software development project, the project manager selects a fixed-price contract for a well-defined module, a cost-plus contract for continuous support, and a time and material contract for additional ad-hoc development.

C. Vendor Management: Ensuring Cost-Effective and Quality Deliverables

Effective vendor management is essential for optimizing project costs and ensuring the delivery of high-quality goods and services. It involves selecting reliable vendors, establishing clear communication channels, and monitoring vendor performance throughout the project.

Key Points:

- Vendor Selection: Careful evaluation of vendors’ capabilities, experience, and cost structures helps in selecting the most suitable and cost-effective vendors.

- Performance Monitoring: Regularly monitoring vendor performance ensures that deliverables meet quality standards and are delivered within agreed-upon timelines and costs.

- Vendor Relationships: Building strong relationships with vendors promotes collaboration and encourages them to provide competitive pricing and excellent service.

Example: In an infrastructure project, the project manager conducts a thorough vendor evaluation, considering factors like past performance, expertise, and cost. After selecting a reliable vendor, they maintain open communication channels and conduct regular progress reviews to ensure the project stays on track.

By effectively managing procurement and considering cost implications, contract types, and vendor relationships, project managers can optimize project costs, reduce risks, and ensure the timely delivery of high-quality deliverables, contributing to the project’s overall success.

VII. Risk Management and Cost Contingency

A. Identifying Cost-Related Risks: Mitigating Cost Overruns

Identifying and managing risks that could impact project costs is a crucial aspect of cost management. Project managers need to proactively identify cost-related risks, assess their potential impact on the project budget, and develop mitigation strategies to prevent cost overruns.

Key Points:

- Cost-related risks may include unforeseen price increases, resource shortages, scope changes, or project delays.

- Regular risk assessments and risk workshops involving key stakeholders aid in the early detection of potential risks.

Example: In a product development project, the project manager identifies a risk of delayed shipment of critical components from a supplier due to a labor strike. To mitigate this risk, they explore alternative suppliers and negotiate flexible delivery schedules to prevent costly delays.

B. Quantitative Risk Analysis: Estimating Cost Contingency Reserves

Quantitative risk analysis involves assessing the probability and impact of identified risks on the project’s budget. It helps project managers estimate cost contingency reserves, which are set aside to address potential cost overruns resulting from unforeseen risks.

Key Points:

- Using data and probability distributions, project managers can calculate the expected monetary value of individual risks.

- The cumulative impact of various risks is considered to determine the total cost contingency required for the project.

Example: In an infrastructure project, the project manager uses historical data and expert judgment to quantify the impact of potential risks, such as weather-related delays and labor disputes. Based on the analysis, they determine a contingency reserve to cover potential additional costs arising from these risks.

C. Integrating Risk Management with Cost Control Processes

Effective cost control requires seamless integration of risk management into the project’s overall management processes. Cost control activities should encompass regular risk reviews, performance evaluations, and corrective actions to ensure that cost contingencies are utilized wisely.

Key Points:

- Risk management should be an ongoing process, integrated into all project phases.

- Regular project performance reviews should include assessing risk responses and updating cost contingency reserves based on project progress.

Example: In an IT project, the project manager holds regular project status meetings with the team and stakeholders. During these meetings, they review identified risks, assess their current status, and update cost contingency reserves based on the project’s progress and risk response effectiveness.

By actively managing cost-related risks, estimating cost contingency reserves, and integrating risk management with cost control processes, project managers can proactively address potential cost overruns, ensure financial discipline, and maintain project performance within approved budgets.

VIII. Sustainable Cost Management Practices

A. Environmental and Social Impact of Project Costs

In the pursuit of responsible project management, sustainable cost management practices recognize the broader environmental and social implications of project costs. Project managers are increasingly mindful of the project’s ecological footprint, social equity, and contribution to a sustainable future.

Key Points:

- Assessing the environmental impact involves considering factors such as carbon emissions, resource consumption, and waste generation throughout the project lifecycle.

- Social impact evaluation encompasses promoting inclusivity, fostering community engagement, and creating opportunities for local development.

Example: In a renewable energy project, the project manager conducts a Life Cycle Assessment (LCA) to analyze the environmental impact from raw material extraction to the project’s end-of-life. Additionally, they engage with local communities, offer job training programs, and prioritize the hiring of local labor, ensuring a positive social impact.

B. Sustainable Cost Reduction: Innovations for Efficiency

Sustainable cost management explores innovative strategies that not only optimize project expenses but also align with eco-friendly practices. Embracing sustainable cost reduction methods fosters efficiency while reducing the project’s environmental footprint.

Key Points:

- Leveraging renewable energy sources, adopting green technologies, and implementing energy-efficient processes contribute to cost savings and environmental benefits.

- Integrating digitalization, automation, and remote collaboration reduces operational costs while promoting sustainability.

Example: In a construction project, the project manager incorporates solar panels for on-site energy generation, uses recycled construction materials, and employs Building Information Modeling (BIM) technology for precise resource allocation and waste reduction. These sustainable cost reduction practices lead to financial savings and a more environmentally responsible project.

C. Long-term Cost Optimization: Benefits Beyond Project Completion

Paragraph: Sustainable cost management looks beyond the project’s immediate horizon and aims for long-term cost optimization. By considering the project’s legacy and future operational expenses, project managers ensure the project’s lasting efficiency and economic benefits.

Key Points:

- Investing in durable, high-quality materials and infrastructure reduces maintenance and replacement costs over the project’s lifespan.

- Fostering continuous employee development and upskilling enhances workforce productivity and minimizes future operational expenses.

Example: In a facility management project, the project manager selects energy-efficient HVAC systems and implements a proactive maintenance plan to extend the infrastructure’s longevity and reduce long-term repair costs. Simultaneously, they prioritize employee training programs to ensure optimal performance and lower operational expenses over time.

By embracing sustainable cost management practices, project managers contribute to environmental preservation, social well-being, and long-term cost optimization. By incorporating responsible and innovative approaches, projects become beacons of sustainability, leaving a positive impact on the world and creating lasting value beyond their completion.

IX. Case Studies: Real-World Examples of Effective Cost Management

A. Success Stories: Projects with Exemplary Cost Management

Examining success stories of projects with exemplary cost management provides valuable insights into how effective strategies and best practices can lead to successful project outcomes. These case studies showcase how prudent cost management has contributed to project success, financial efficiency, and achievement of project objectives.

Key Points:

- Success stories demonstrate how adherence to budgetary constraints and proactive cost control measures led to on-time and within-budget project delivery.

- Projects that effectively managed risks, utilized cost-saving techniques, and embraced sustainability practices are featured in these case studies.

Example: A large-scale infrastructure project was completed on time and within the allocated budget due to meticulous cost estimation, effective procurement practices, and continuous risk monitoring. The project team implemented innovative construction methods, reducing material waste and associated costs, and collaborated closely with stakeholders, ensuring timely approvals and smooth execution.

B. Lessons Learned from Cost Management Challenges

Learning from cost management challenges in real-world projects is essential for avoiding common pitfalls and improving future cost management practices. These case studies highlight the obstacles faced, the impact of cost overruns, and the importance of adapting strategies for dynamic project environments.

Key Points:

- Case studies of projects that encountered cost management challenges illustrate the consequences of inadequate risk identification and contingency planning.

- Lessons learned emphasize the need for regular monitoring, agile budget adjustments, and swift corrective actions to maintain cost control.

Example: A software development project faced cost overruns due to unexpected changes in client requirements and scope creep. The lack of a comprehensive change control process resulted in cost escalations and project delays. The project team later implemented a rigorous change management system, conducted regular risk assessments, and maintained open communication with the client to prevent similar challenges in subsequent projects.

By examining real-world case studies of successful cost management and learning from challenges faced, project managers can gain valuable insights to enhance their own cost management practices. These examples inspire prudent financial decisions, risk mitigation strategies, and a commitment to delivering projects with excellence while achieving financial objectives.

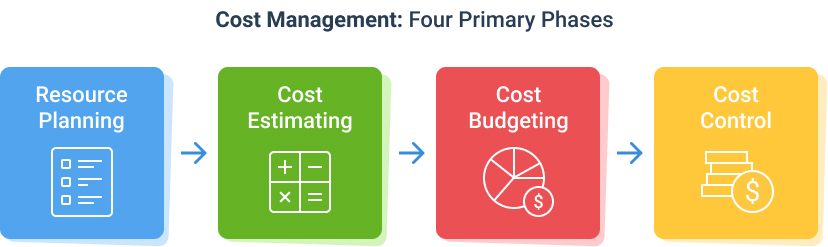

X. Cost Management: Steps, Basics, and Benefits

Steps in Cost Management:

- Cost Estimation: Cost estimation is the process of approximating the total expenses required to complete the project successfully. It involves analyzing the project scope, identifying necessary resources, and determining their associated costs. Different techniques like analogous estimating, parametric estimating, and bottom-up estimating are used to arrive at accurate cost estimates.

- Cost Budgeting: Once cost estimates are available, project managers create a detailed budget that allocates funds to specific project activities. The budget outlines how much money is allocated to labor, materials, equipment, and other expenses at each stage of the project.

- Cost Control: Cost control involves monitoring and managing project expenses during execution to ensure they align with the budget. Regular tracking of actual costs against the budget allows project managers to identify cost variances early and take corrective actions if needed.

- Cost Optimization: Continuous efforts are made to optimize project costs throughout its lifecycle. Project managers explore cost-saving opportunities, implement process improvements, negotiate with vendors, and leverage innovative technologies to enhance cost efficiency without compromising quality.

Basics of Cost Management:

- Resource Allocation: Cost management involves strategic allocation of resources to maximize productivity and minimize expenses. Proper resource allocation ensures that the right resources are available at the right time, avoiding delays and inefficiencies.

- Risk Assessment: Identifying potential risks that could impact project costs is a crucial aspect of cost management. Risk assessment involves analyzing both internal and external risks, quantifying their potential impact, and developing contingency plans to manage them effectively.

- Earned Value Management (EVM): EVM is a performance measurement technique that integrates cost, schedule, and work progress data to assess project health. It provides valuable insights into project cost and schedule variances, helping project managers make informed decisions.

- Change Management: Change management processes are essential in cost management to address any scope changes that might impact project costs. Formal change control procedures ensure that any alterations to the project scope are thoroughly evaluated for their financial impact.

Benefits of Cost Management:

- Financial Control: Cost management ensures that projects stay within budgetary constraints, allowing organizations to maintain financial control and avoid unexpected financial burdens.

- Resource Efficiency: Efficient resource allocation through cost management minimizes waste and optimizes resource utilization, enhancing overall project productivity.

- Project Success: Successful cost management leads to on-time and within-budget project completion, contributing to higher project success rates and customer satisfaction.

- Risk Mitigation: By proactively managing costs and identifying potential risks, cost management helps organizations mitigate financial risks and improves project resilience.

- Strategic Decision Making: Cost management data facilitates data-driven decision-making, guiding project managers in prioritizing tasks, allocating resources, and adapting to changing project needs.

- Competitive Advantage: Organizations that excel in cost management can offer competitive pricing, making them more attractive to clients and stakeholders in the market.

In conclusion, cost management is a vital aspect of project management that involves estimating, budgeting, monitoring, and optimizing project expenses. By following the detailed steps of cost management, understanding its basics, and leveraging its numerous benefits, project managers can ensure financial discipline, resource efficiency, and successful project outcomes. Proper cost management empowers organizations to achieve their objectives while maintaining financial stability and competitiveness in a dynamic business environment.

XI. Conclusion

A. The Key Role of Cost Management in Project Success

Cost management plays a pivotal role in the success of any project. It is a dynamic process that involves estimating, budgeting, monitoring, and controlling costs to ensure the project’s financial health. Effective cost management empowers project managers to make informed decisions, optimize resource allocation, and prevent cost overruns, ultimately leading to successful project outcomes.

Key Points:

- Cost management ensures that projects stay within budgetary constraints and financial targets, enhancing the project’s overall profitability.

- Proper cost management enables project managers to allocate resources efficiently, minimize financial risks, and achieve project objectives.

B. Embracing Cost Management Best Practices for Sustainable Project Outcomes

Embracing cost management best practices is essential for achieving sustainable project outcomes. By integrating sustainable cost reduction techniques, leveraging cost-benefit analysis, and integrating risk management, project managers can drive efficiency, reduce waste, and promote responsible resource usage.

Key Points:

- Sustainable cost management practices consider not only financial factors but also environmental and social impacts, contributing to a more responsible and ethical project approach.

- Adopting innovative technologies, robust procurement strategies, and long-term cost optimization plans ensure projects deliver value beyond completion.

In conclusion, effective cost management is not just about financial control; it is a strategic discipline that drives project success and fosters sustainable growth. By consistently evaluating cost drivers, estimating contingency reserves, and making data-driven decisions, project managers can achieve successful project outcomes while promoting environmental responsibility and social well-being. Embracing cost management best practices empowers project teams to navigate uncertainties, embrace opportunities, and deliver projects that leave a positive impact on stakeholders, communities, and the world at large. With prudent financial management and a commitment to sustainability, projects can thrive, even in dynamic and challenging environments.

{kind=link}